All Posts

5 min read

How cumulative accounting benefits your carbon farming project

Published on

February 12, 2026

Author

Tobias Horstmann

Chief Product Officer

.png)

Julian Kremers

Co-founder and CSO

Erik Scharwächter

Lead Data Scientist

Emily Nielsen

Product Marketing Manager

Sections

Version 3 of Verra’s VM0042 offers clarity and practical changes to the soil carbon projects on the voluntary carbon market. The new version, co-authored by Seqana and Terracarbon, aims to uphold or improve the scientific rigor and the project economics of carbon projects while considering the practical implementation of Measurement, Monitoring, Reporting and Verification (MMRV).

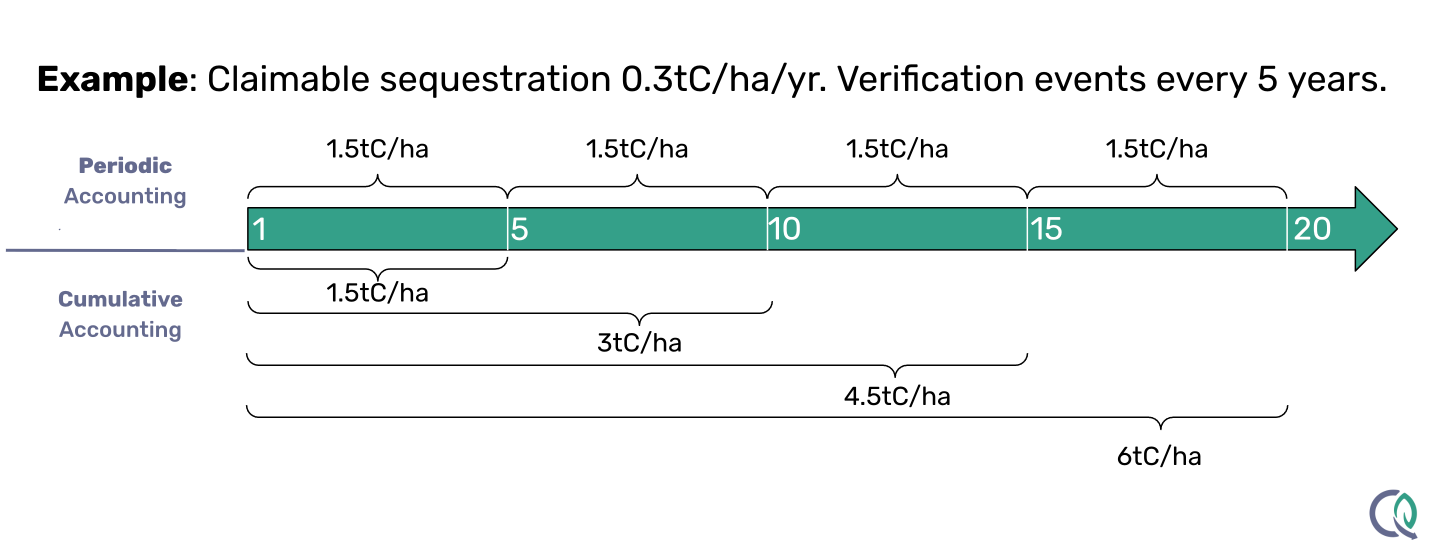

One of the most impactful topics is the introduction of cumulative accounting for carbon projects. Cumulative accounting uses the total amount of sequestered carbon since the project began when calculating sample sizes and uncertainty deductions rather than the marginal change between verification events as used in periodic accounting, the standard approach prior to this latest version.

In this blog post, we’ll discuss cumulative accounting, the impacts it has on your carbon project, and how cumulative accounting is beneficial to your carbon project.

What is cumulative accounting?

Cumulative accounting allows project developers to consider the total cumulative SOC stock change since the project started when calculating the sample size or uncertainty deductions. Previous versions of VM0042 required project developers only account for SOC stock change from the previous verification event, rather than the entire project duration. Verification events occur when Validation and Verification Bodies (VVBs) audit and approve the outcomes of a project for a given time period.

The example above demonstrates how a project developer will use the total amount of carbon sequestered as time goes on throughout the project, as opposed to being limited to the carbon sequestered during the previous verification event. This higher amount of sequestration enables the project developer to reduce the uncertainty deductions throughout the project duration without compromising the scientific rigor of the sequestration claims. Alternatively, project developers also have the option of reducing sample sizes while maintaining constant uncertainty deductions.

The financial benefit of cumulative accounting on your project

To illustrate the positive financial implications of cumulative accounting across soil carbon projects, let’s first walk through a simplified example under Measure and Remeasure, without the use of Digital Soil Maps (DSMs).

Assumptions

- Annual sequestration rate: 0.3 tC/ha/year

- Verification frequency: every 5 years

- Project duration: 20 years

- SOC stock variance of change: 200 tC²/ha²

- Paired sampling

- Carbon credit price: 40 €/tCO₂e

Under cumulative accounting, project developers can choose between three strategic levers over the lifetime of the project:

- Reduce uncertainty deductions while keeping the sample size constant,

- Reduce the required sample size while maintaining uncertainty deductions,

- Combine both approaches, resulting in a smaller reduction in sample size and a smaller reduction in uncertainty deductions.

Each option affects project economics differently, and the best approach for the project depends on the developer’s priorities and cost structure.

Option 1: Reduce uncertainty deductions at a fixed sample size

Let's assume you maintain a constant sample size of 500 for every sampling campaign which results in an absolute uncertainty deduction of 1 tCO₂e/ha for the example project scenario following VM0042 formulas. The financial difference between projects using periodic accounting or cumulative accounting is as follows:

- Periodic Accounting (Previous versions of VM0042): You subtract 1 tCO₂e/ha at each of the 4 verification events. Over 20 years, this totals 4 tCO₂e/ha in deductions, which translates into 160€/ha lost in value over 20 years due to uncertainty deductions, assuming a credit price of 40 €/tCO₂e.

- Cumulative Accounting (VM0042 Version 3): The uncertainty deduction (1 tCO₂e/ha) is subtracted only from the cumulative sequestration total. Over 20 years, your total deduction remains just 1 tCO₂e/ha. This results in a revenue loss of only 40€/ha. With cumulative accounting, the absolute uncertainty (expressed as tCO2e/ha or their total monetary value) remains constant throughout the project lifecycle. As cumulative sequestration increases over time while absolute uncertainty remains unchanged, the relative uncertainty deduction (expressed as a percentage) declines.

Result: In this scenario, cumulative accounting saves the project developer 120€/ha in revenue due to lower uncertainty deductions over the 20 years project duration.

In the project example above, cumulative accounting applies uncertainty deductions in year 5 for the first verification event. This example assumes that the variance of SOC stock change and the sampling design remaining constant over the project life-cycle, and so the absolute uncertainty deduction at this first remeasurement will be large enough to completely cover the absolute uncertainty of subsequent remeasurements. The subsequent relative uncertainty will decrease as the cumulative sequestration will increase. While uncertainty still needs to be estimated and subtracted from the subsequent cumulative estimates at every remeasurement, it will effectively result in 0 additional uncertainty deductions beyond the first verification event since the maximum cumulative absolute uncertainty for the entire project lifetime is applied at the first verification event already.

Optimizing for uncertainty deductions at a fixed sample size tends to be economically superior to reducing sample size while maintaining uncertainty deductions. In order to help teams determine the ideal sample size for your unique project, we’ve created the Economic Optimum Number of Samples (EONS) calculator. The goal of the EONS calculator is for teams to experiment with how various sample sizes impact the long term project economics.

Projects can also improve your stratification or apply Model-Assisted Estimations to even reduce your cumulative uncertainty. This allows project proponents to recover some of the revenue previously lost to uncertainty deductions in subsequent verification events.

Option 2: Reduced sample size while maintaining uncertainty deductions:

Cumulative accounting also enables a second lever: reducing sampling intensity while keeping uncertainty deductions constant. If we keep sample size at a constant to achieve 90% power and 5% significance (see MDD approach to calculate sample size), conceptually, cumulative accounting increases the MDD. For paired sampling, this leads to the following effect on reduced sample size requirements over the course of a 20 year project.

Key takeaway: Cumulative accounting allows projects to scale down sampling costs over time without resulting in higher uncertainty deductions.

Note: For independent sampling, the effect is slightly different. Reach out to Seqana to learn more.

Option 3: Combine both approaches, resulting in a smaller reduction in sample size and a smaller reduction in uncertainty deductions.

Often projects will use a combination of both approaches in order to best align with their specific project needs. Considerations such as short term vs long term cash flow or reaching a necessary sampling density to provide farmers with ground truth data may factor into how you choose to optimize your approach. Finding the right balance of uncertainty deduction vs sample size optimization is based on project goals.

Cumulative accounting with Biogeochemical models (BGCMs) or Digital Soil Maps (DSMs)

The implications for projects using BGCMs, sometimes called Process Based Models (PBMs), or DSMs are more nuanced. Depending on the model’s performance after recalibration, cumulative uncertainty deductions may increase, decrease, or remain unchanged. In most cases, the direction, magnitude and cadence of change in cumulative uncertainty differ significantly between BGCMs and DSMs. Reach out to our team to explore how cumulative accounting applies to your BGCM and DSM projects through bespoke consulting.

How does cumulative accounting mitigate the risk of overestimating sequestration?

Cumulative accounting also improves scientific integrity under Measure and Model when BGCMs are used. At the start of a project, biogeochemical models (BGCMs) are calibrated and validated using external datasets (i.e., data from outside the project area). The BGCM performance is then re-assessed after the first remeasurement campaign (the BGCM true-up), which can reveal whether the BGCM has overestimated sequestration and whether the uncertainties are higher than originally anticipated.

Previously, without cumulative accounting, if a BGCM overestimated sequestration, project proponents generally only needed to adjust future projections, without correcting credits already issued. Under cumulative accounting, this changes: any overestimated sequestration must be fully compensated through new sequestration before additional credits can be issued.

For example, if the BGCM overestimated sequestration in the previous verification period by 0.2 tC/ha, the project must first sequester that 0.2 tC/ha before it can start issuing new credits for any additional sequestration in subsequent periods.

This is a clear win for the scientific integrity of SOC projects, but it also introduces a planning consideration for project developers: if BGCMs overestimate sequestration early on in the project and/or underestimate the uncertainty, cumulative accounting can lead to time periods of not generating any revenue while continuing to have costs for keeping the project running.

What does cumulative accounting mean for my project?

If you are registering your project with Verra’s VM0042.v3, cumulative accounting applied. Specific guidance on cumulative accounting for your project can be found in Section 8.3 of VM0042.v3.

Regardless of whether you use Measure and Model or Measure and Remeasure to quantify SOC change, and whether or not you apply a Digital Soil Maps, Seqana provides tailored guidance on how cumulative accounting affects your project’s economics and risk profile, and supports you in defining the optimal MRV strategy. Reach out to our experts at Seqana.

© 2025 Seqana. All rights reserved.